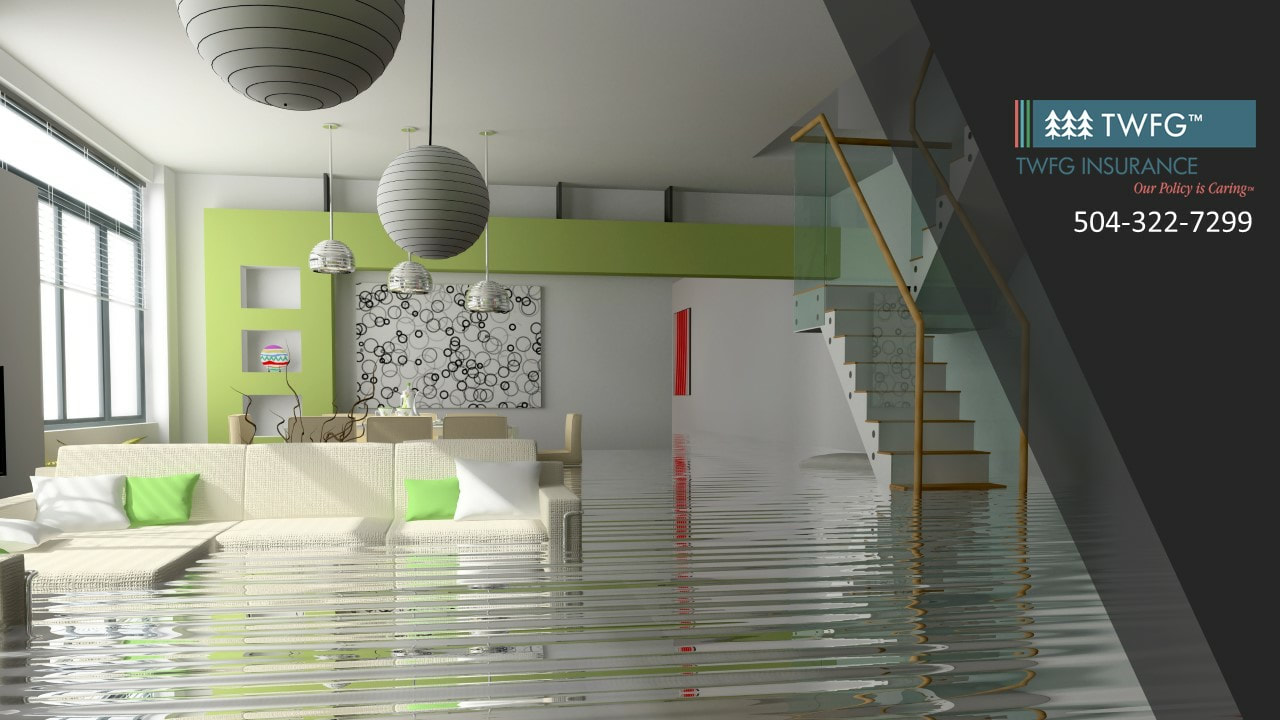

Heavy rain, storm surge, hurricanes and other severe weather events can lead to devastating floods that cause extensive damage. According to the Federal Emergency Management Agency (FEMA), flood damage totaled over $8 billion in 2017 and many of the affected areas are still recovering from the impact.

After a flood hits your business, you’ll still have expenses such as building leases, employee payrolls and cleanup costs. And because any business interruption means that your revenue will be lowered or gone altogether, you’ll need a source of income quickly. Although flood insurance is there to help you recover and rebuild your business, you need to know how to make a claim so that you can get all of the coverage you can as soon as possible. Starting the Claims Process You can start the claims process immediately after a flood. However, before you call us at (504) 322-7299 you should make sure you have the following information:

When the insurer that issued the flood policy gets notice of your loss, you may be able to qualify for an advance payment before the inspection. However, these payments are at the discretion of the insurer and shouldn’t be relied on when you’re planning your recovery process. Pre-inspection Steps After the claims process has started and local officials have determined that it’s safe, you should return to your property to prepare for an inspection to assess the damage. Here are some steps to take before an inspection:

Once a claims adjuster arrives to inspect your business, make sure to record their contact information. After walking through the National Flood Insurance Program’s claims process, the adjuster will inspect your property and take measurements and pictures of the damage. If an adjuster finds that your business has extensive damage, you may qualify for an accelerated claims process to help you begin repairs immediately. Your adjuster may also have advice for you based on your specific policy. Making Repairs and Other Resources When working with contractors, vendors and third parties after a flood, it’s important to keep copies of all receipts, bank statements, invoices and other documents that show how you paid for repairs. These items may be used as permanent records in case your business floods in the future, and they could affect how much you’re compensated. Getting your insurance coverage after a flood is key, but you have other resources at your disposal. FEMA’s website has a number of resources and programs you can use to recover. You can also contact TWFG Insurance - Tony Voiron for any questions on your flood policy or for resources to help you reduce your damage with pre-incident plans.

1 Comment

A new year brings new issues for HR professionals to contend with. Some challenges are similar to previous years (overtime uncertainty), while others are more unique and complicated (legal marijuana and employment). Despite inherent difficulties, staying tuned in to these six trends can keep you ahead of the game in 2019. Ignoring them will only put you behind.

Below are the top trends to monitor in the coming months. 1. Opioids, Marijuana and the Workplace Opioids have been concerning employers for the last few years, and quietly ravaging the country for even longer. In 2017, the opioid crisis was declared a national emergency due to tens of thousands dying each year from prescription painkillers. Many of these tragedies started with a legal prescription after a common medical procedure. Beyond their deadly risks, opioids also cause absenteeism and performance issues in the workplace. Opioids are difficult to detect in a drug test and even harder to perceive without one. Knowing this, it’s critical to modernize your drug policy to address opioids and offer resources for alternative pain management strategies. Legal marijuana is also complicating drug policies. Similar to opioids, marijuana is increasingly difficult to detect, with the growing popularity of oils and edibles. Moreover, the drug is legal for medical use in 30 states, making testing legally tricky. You may find it easiest to adjust your drug policy to focus on workplace performance. For instance, clearly prohibiting impairment at work or the promotion of drug use through paraphernalia. Adopting a zero-tolerance policy may backfire with state laws, so be sure to have legal counsel review your policy before enforcing it. 2. Leave-related Issues Did you know that 47 percent of employers were very challenged by cross-state leave laws and 43 percent found it extremely difficult administrating leaves in general, according to a recent XpertHR survey? With ever-expanding legislation, it’s not too surprising. Multistate businesses must contend with different state laws, but even smaller employers can find themselves juggling laws between localities. Without proper guidance, handling common requests like family leave, sick time and reasonable accommodation under the Americans with Disabilities Act can be a nightmare. The first thing employers must do is determine which leave laws apply to them, remembering that certain localities might have different rules. Other aspects, like which leaves can be used concurrently and proper leave documentation should come next. And, of course, proper employee communication is a must—not just putting policies in a handbook, but posting leave notices as well. 3. Soaring Health Care Costs Paying over $15,000 annually for each employee’s health care in 2019 sounds like a bad dream, but it’s the real cost trend. With rates surpassing $680 and $20,000 for single and family coverage, respectively, employers are scrambling to cut costs wherever they can. Yet, that can be easier said than done. Some organizations are encouraging workers to utilize telemedicine or virtual care as a way to trim costs. By “visiting” a doctor online for minor health issues, patients can save a trip to the hospital. And, since it’s virtual, everyone saves money. Another cost-saving strategy is the consumer driven health plan (CDHP) model. This strategy empowers employees to control their health care decisions and choose care that best suits them. Since employees use a savings account to help offset costs from their high deductible health plans, they are incentivized to pick more affordable options. 4. Wage and Hour Concerns Hire more workers or pay overtime? That’s the question growing businesses must ask themselves. With overtime changes looming in the first quarter of 2019, you may think it’s easier to hire more workers at lower salaries. But, depending on your situation, that may not be true. Many states are primed to raise their respective minimum wages in 2019. What’s more, the majority of those rates are already higher than the federal minimum. If you’re considering hiring more workers, check to make sure you know how much you’ll have to pay them in your state. The same goes for federal contractors. As for salaried employees, it looks like we won’t know anything about the overtime rule until at least March 2019. This leaves the current overtime threshold at $23,660. Experts expect that number to increase to between $32,000 and $35,000—far lower than the $47,476 rate initially proposed in 2016. This means you should keep watching for regulatory updates in the coming months. 5. New Technologies HR is always looking for new ways to streamline and improve its processes. In 2019, it appears that people analytics and recruiting technologies will be at the forefront of the trend, according to professional HR organization Toolbox. People analytics is a way of tracking things like employee engagement data, training program effectiveness or ad placement success. The practice examines human data and crunches the numbers so you have a better idea of the return on investment. Need to know if your employees feel appreciated? Want to discover which methods employees are using to communicate with each other? This is where people analytics can help. TWFG Insurance Tony Voiron - Business Insurance, Metairie, LA - 504-322-7299  Maybe you've never heard of umbrella insurance -- it's not advertised much, and unlike car and homeowners insurance, no one requires you to carry it. But it's something everyone should consider because, for a low premium, it gives you a ton of financial protection against bad luck and unreasonable people.

What is Umbrella Insurance? Also called excess liability insurance, this policy works with your auto and homeowners or renters insurance. Essentially, it makes sure you're thoroughly protected financially if you're found responsible for injuring another person and a court decides you should pay the resulting expenses. What does "regular" insurance cover, then? Your primary insurance (that's your auto, homeowners or renters insurance) typically provides some liability coverage and might be enough to pay for all the damages resulting from a minor incident. However, it probably won't be enough to cover the repercussions of a more severe unexpected accident. Who should consider umbrella insurance? Umbrella policies aren't just for wealthy people with lots of assets. Could you afford to lose all the money you've saved, even if it's only a modest sum? And if you don't have any assets to seize, or if your assets aren't valuable enough, umbrella insurance will protect you from having your wages garnished. What does it cover? Umbrella insurance typically covers things like third-party claims for medical care, lost wages, pain and suffering, and attorney's fees. And it doesn't just cover you, the policyholder; it covers everyone in your household. Having a teenage driver is a good reason to have umbrella insurance, for example. Call TWFG Tony Voiron for your quote today 504-322-7299.  With holiday travel and extreme weather in our near future, we thought it would be a good time to share extreme weather driving tips with the new drivers in your household.

RAIN AND THUNDERSTORMS • Turn on your headlights, wipers, and defroster on to increase visibility. • Drive in the tracks of the vehicle ahead of you and reduce your speed. • Allow for increased space between your vehicle and the one in front of you. • If you hydroplane, hold the steering wheel straight and remove your foot from the gas. SNOW, SLEET AND FREEZING RAIN • Clean ice and snow off your windows, hood, and trunk before departing. • Drive with extreme caution and at reduced speeds. • Do not brake quickly as you may spin out of control. FOG • Slow down before you reach a patch of fog in front of you. • Use only your low beams or fog lights and put on your defroster and wipers to increase visibility. • If the fog is extremely thick, roll down all of your windows to hear other vehicles around you. Feel free to share with friends that have new drivers in their household. TWFG Insurance Tony Voiron | 504-322-7299 | www.twfglouisiana.com  Halloween is an exciting time of year for kids, and to help them have a safe holiday, here are some tips from the American Academy of Pediatrics (AAP).

ALL DRESSED UP:

HEALTHY HALLOWEEN:

©2018 American Academy of Pediatrics  On Oct. 9, 2018, the Department of Labor (DOL) announced that its Wage and Hour Division (WHD) recovered a record $304 million in wages owed to workers in fiscal year (FY) 2018. In comparison, the WHD recovered $270 million in back wages in FY 2017.

Compliance Assistance The DOL’s secretary, Alex Acosta, states that the recovered wages are a demonstration that the DOL and WHD are committed to ensuring workers receive the wages they deserve. Moreover, the WHD’s compliance assistance efforts demonstrate its commitment to helping employers meet compliance requirements. Specifically, in FY 2018, the WHD held 3,643 educational outreach events to help job creators understand their responsibilities under the law. PAID Program Extension On the same day, the WHD also announced a six-month extension of the voluntary Payroll Audit Independent Determination (PAID) program. This program is an initiative designed to help expedite back wage payments to workers. Without this program, workers may have to wait for investigations and court cases to be resolved or concluded. What does this mean for my organization? Complying with wage and hour regulations should be a priority for your organization. This is especially important as the DOL has demonstrated that it will focus on ensuring compliance, as seen by the record numbers it has collected recently. With more employees working remotely, using their smartphones to access email or work at home, and looming overtime rule changes in 2019, now is the time to ensure your organization’s compliance. Contact TWFG Insurance - Voiron Insurance Services today for help complying with wage and hour regulations, or for additional resources.  Did You Know?

One of the most common homeowners insurance claims is completely preventable. It’s not fires or theft; it’s water damage. This is not damage due to flooding, heavy rainstorms or snow on the roof – rather, it’s due to simple maintenance tasks that are often ignored or go unnoticed. Use these tips to help prevent water damage:

Prevention Pays How does water damage occur? It’s simple: homeowners fail to check the connection between the water line and their washing machine or other similar appliances. Eventually, the connection fails, and water leaks into the home until someone discovers the mess. Do a quick check of all your water lines from time to time, especially in low-traffic areas of the home. If you notice anything suspicious, contact a licensed professional to come take a look immediately.  On Sept. 28, 2018, Facebook announced that nearly 50 million user accounts were compromised in a data breach. The breach, which can be traced back to July 2017, is one of the largest in the company’s 14-year history.

While investigations are ongoing, the company said hackers exploited a software vulnerability in Facebook’s "View As" feature to steal access tokens and gain control of user accounts. Access tokens are effectively digital keys to specific accounts, and stealing them allows attackers to view private posts or compose status updates without the knowledge of the affected user. In addition, the attack allowed the hackers to see anything that users can see on their own profile, including the names and birth dates of friends and family members. Such information could be used in future phishing attacks. In response to the attack, Facebook reset 90 million logins automatically, fixed the software vulnerability and informed law enforcement officials. While the company says that users do not need to change their passwords, individuals experiencing login issues should navigate to Facebook’s Help Center. As a safety precaution, users are encouraged to log in and out of all of their accounts on every device. Users can see all of the devices they’re currently signed into here. To learn more about the breach, read Facebook’s official blog post.  If you’ve had a fire, water damage or another unfortunate event in your home, don’t fret. We have all the information that you need to get your claim underway so you can get your life back to normal. When you have a homeowners insurance claim, your actions can make all the difference. Here’s how to maneuver through the claims process with ease:

Let us help you throughout the process—contact TWFG Insurance - Voiron Insurance Services, LLC if you have questions or concerns.  Know The Risks and Be Prepared

Many people do not realize just how dangerous fireworks and sparklers can be—which is a primary reason that injuries occur. Fireworks can not only injure the users but can also affect bystanders. Most injuries and accidents occur because people often underestimate the dangers posed by fireworks and don’t take proper safety precautions. In fact, the Consumer Product Safety Commission found that more than half of fireworks-related injuries were the result of unexpected ignition or consumers not using fireworks as intended. Unfortunately, all fireworks carry potential risks of burns, blindness and other injuries, but you can significantly reduce the potential for danger through proper planning and safety. Tips for Safe Firework Use When using fireworks, always plan in advance who will shoot them, and what safety precautions will be in place. Here are some suggestions to ensure safety and avoid accidents: • Keep spectators at a safe distance. • Never give sparklers to children under five. • Only use fireworks as intended. Do not alter or combine them, and do not use homemade fireworks. • Do not carry fireworks in your pocket or shoot them from metal or glass containers. • Point fireworks away from people, homes, trees, etc. • Show children how to properly hold sparklers, how to stay far enough away from other children and what not to do; throw, run or fight with sparkler in hand—and always supervise closely. • Always have a hose or water bucket handy. • Never try to relight a dud (a firework that didn’t properly ignite). • Soak all firework debris in water before throwing it away. • Use fireworks and sparklers outdoors only. • Wear safety goggles when handling or shooting off fireworks. • Do not shoot fireworks off while under the influence of alcohol. Take Precautions, Reduce Risk Be sure that your celebrations comply with all applicable state and local laws. The laws regulate who can purchase and use fireworks, when they can be purchased and used, and what the maximum noise levels may be. Under these regulations, the focus is not only on product safety but also on the reduction of accidents and injuries to you the consumer. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

April 2020

Categories |

RSS Feed

RSS Feed